Car insurance prices continue to climb as we enter Q2 of 2024 for a multitude of reasons that consumers and insureds have a hard time understanding. As responsible consumers that have had few to no claims over the many years, it is frustrating to see insurance premiums increase seemingly paying the price for the actions of others. Unfortunately, there are many factors that contribute to the rise in premiums thus we hope that the following will provide some insight and perspective of the industry and the markets serving your insurance needs.

It is advised to review and assess your insurance needs annually to fully understand your exposure and risks. More importantly, insurance is a financial decision and mitigating risks while making prudent decisions and striking a balance to protect your assets are critical in a pronounced “hard” insurance market!

Let the professionals of St. Louis Insurance Services conduct a review and provide you an assessment of your current coverages and see what we can do to serve your needs! Midwestern insurance professionals are willing to identify the key aspects of your insurance and balance the “what and how” of all things insurance!

www.stlouisinsuranceservices.com

314-288-2880

5 Factors That Contribute to Higher Auto Insurance Rates

Car insurance companies don’t raise rates arbitrarily. To ensure that they can pay out claims, auto insurers must charge enough to cover damages without dipping into reserves. With increasing costs across various parts of the automotive industry, from higher average repair costs to continuing supply chain issues, auto insurance companies have needed to raise rates to turn a profit.

Here are the five key factors that have contributed to increased car insurance rates:

1. Record Inflation Rates

It’s no secret that since the COVID-19 pandemic, inflation has skyrocketed. The Federal Reserve raised rates 11 times between 2022 and 2023 in an attempt to cool soaring prices. The plan generally worked, with inflation decreasing from its record high of 9.1% in June 2022 to a rate of 3.4% in December 2023.

When inflation rises, however, so do prices, and cost increases tend to get baked into the economy whether inflation drops or not. If everything is more expensive, companies pass extra costs on to consumers. As inflation begins to drop, maintaining higher prices is a good way for companies to regain lost profits.

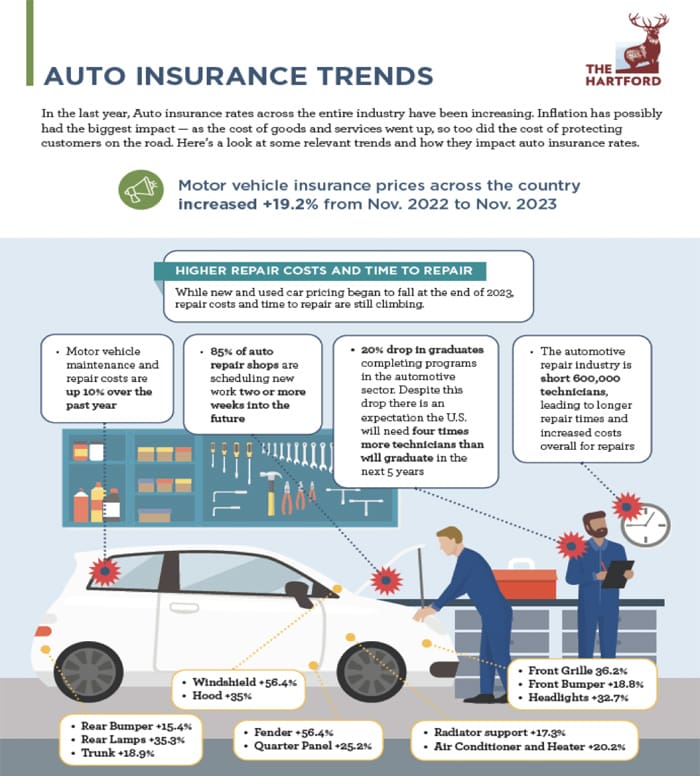

2. Increasing Car Repair Costs

The cost of vehicle maintenance has increased almost 36% over the past five years. Expensive cars like luxury vehicles and high-end sports cars — those with higher repair costs to begin with — were always pricier to insure. But now that repair costs have increased across the board, insurance companies have begun to quickly hike rates to keep up.

3. Recovering Supply Chains

When the COVID-19 pandemic began in 2020, global supply chains shuddered and snapped in response. Carmakers had to put production on hold and parts manufacturers saw orders decrease, leading many plants to shut down permanently. A global chip shortage contributed to significant slowdowns in automotive production as well, and all of this led to a surge in automobile prices.

The United Auto Workers (UAW) strike in the fall of 2023 affected supply chains once again, especially concerning parts manufacturers. As workers walked off the job, production at many of the Big Three’s plants came to a standstill. The result was a decrease in parts orders, which in turn led to additional small businesses laying off workers or closing altogether. This has contributed to increased costs for vehicle replacement parts and equipment.

4. Higher Health Care Costs

Rising health care costs affect auto insurance rates in more ways than most drivers realize. Many states require drivers to hold medical payments coverage (MedPay) or personal injury protection (PIP). These coverages help to pay for medical expenses that result from car accidents.

Data from the Centers for Medicare and Medicaid Services shows that health care spending in the U.S. increased by 10.6% in 2020, 3.2% in 2021 and 4.1% in 2022. As health care becomes less affordable, auto insurance companies charge more for these coverages to compensate.

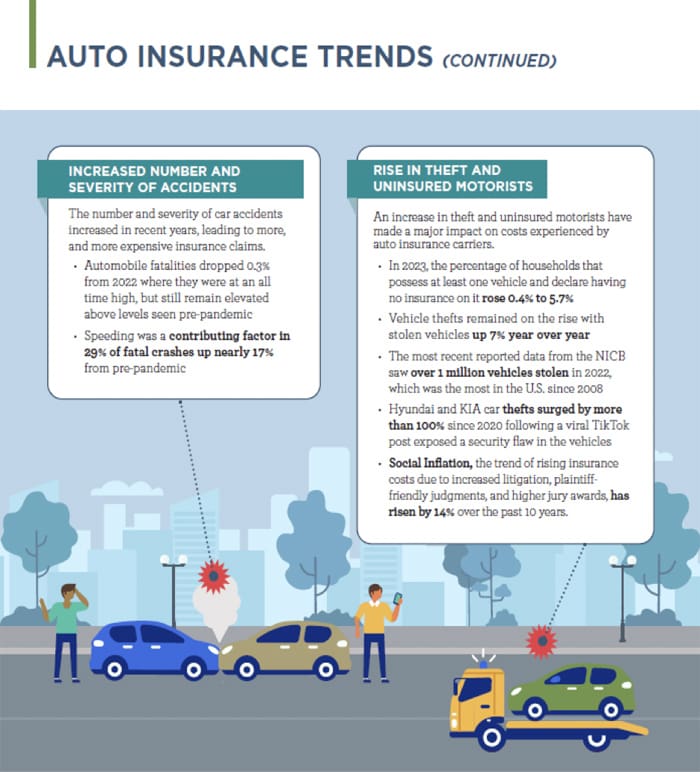

5. Climate Change

Climate change is a huge and steadily growing factor in the increase in auto insurance prices. As weather patterns become more unpredictable, insurers will increase the cost of policies to compensate for the increase in weather-related damage. Some may even stop offering car insurance in certain areas altogether.

For example, in Florida, the increase in flooding events due to hurricanes and other inclement weather led several companies to discontinue services. The providers that remain in Florida can then raise prices due to decreased competition for a product that’s required for all Sunshine State drivers.

As catastrophic climate events like forest fires, snowstorms and flooding occur more regularly, expect insurance providers to react by raising rates.